Last week, the National Institute on Retirement Security (NIRS) released a report that shows how financial asset inequality contributes to the retirement security crisis.

NIRS’s research examined the ownership of financial assets by class and race among the members of Generation X and the baby boomer and millennial generations. They based their definition of what constitutes a financial asset on the Survey of Consumer Finances, which states that it “consists of liquid assets, certificates of deposit, directly held pooled investment funds, stocks, bonds, quasi-liquid assets, savings bonds, whole life insurance, other managed assets, and other financial assets.” These assets can be important for one’s retirement security, but NIRS illustrated that “the majority of Americans own few financial assets that they can save and invest for their retirement.”

The report revealed that there is a troubling divide between the wealthiest members of each generation and lower-wage earners. Across each generation surveyed, the top 25 percent of households by net worth owned the vast majority of financial assets, with the top 25 percent owning 91 percent of assets for baby boomers, 89 percent for Generation X, and 76 percent for millennials as of 2019.

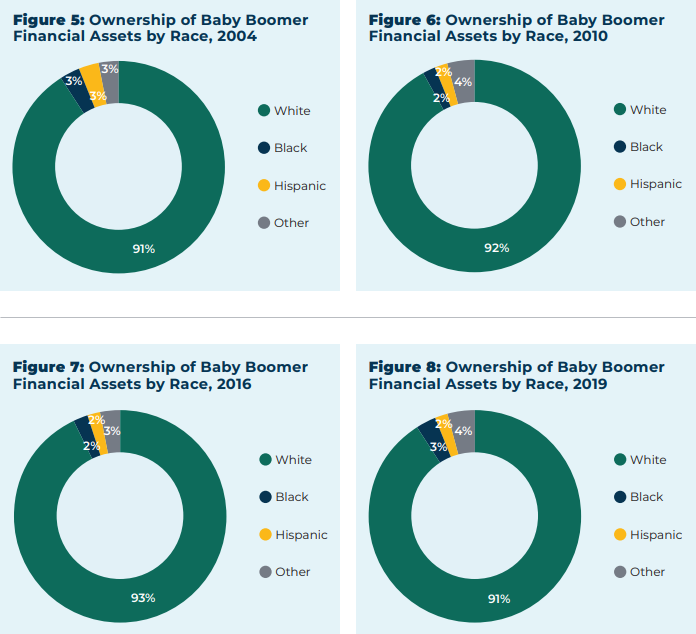

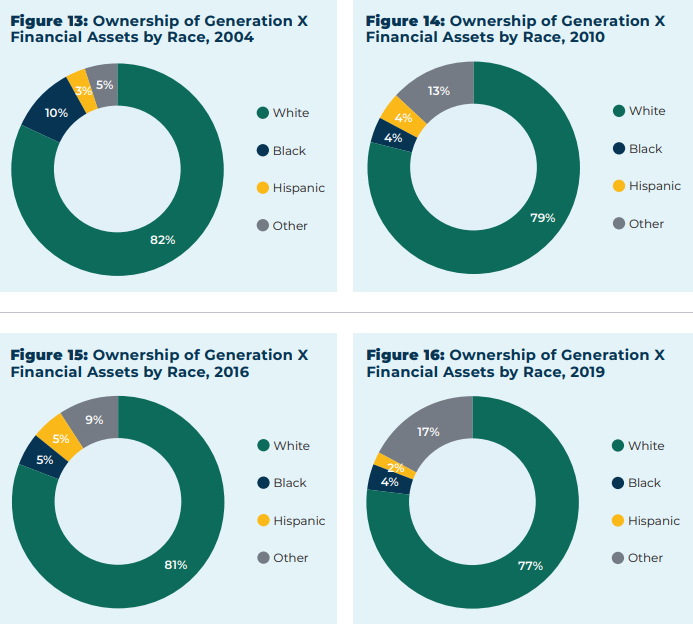

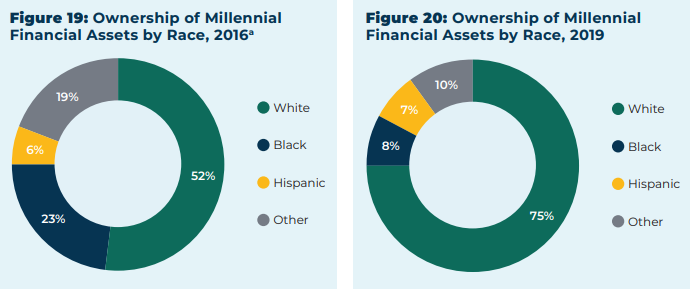

NIRS also found that significant disparities exist between white Americans and Black and Hispanic Americans in the ownership of financial assets. White Americans represent 74 percent of baby boomers, 63 percent of Generation X, and 59 percent of millennials as of 2019, yet they own a disproportionate share of financial assets in each cohort. According to NIRS, 91 percent of white baby boomers, 77 percent of white members of Generation X, and 75 percent of white millennials own financial assets as of 2019, compared with lower numbers of ownership for Black and Hispanic Americans in each generation.

In the solutions section of its report, NIRS identified several bright spots that can improve most working people’s outlook on their retirement. One of them includes protecting pensions, as they “are a vital source of retirement income for many middle-class families” and “help to keep many middle-class families in the middle class throughout retirement.” They help ensure public employees retire with the security and dignity they deserve in retirement.