This year and last year, many have used the term cost-sharing when referring to certain types of pension policy. In particular, Pew Charitable Trusts has been advocating for cost-sharing in pension plans across the nation using pension plans in Tennessee, Wisconsin, and South Dakota as examples of effective policy. Unfortunately, for many pension plans, cost-sharing will mean an increase in employee contributions, hurting communities and hard-working public employees. Additionally, in the long-term, pension plans cost significantly less than switching to a cost-sharing model, which includes 401(k) or hybrid retirement plans.

For the purpose of this blog, let’s take a look at Tennessee.

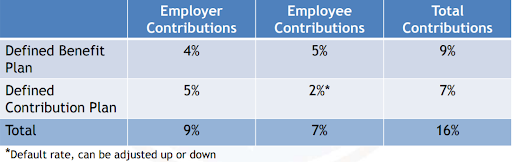

In 2013, Tennessee closed off their defined benefit pension fund to newly hired public employees and opened a hybrid-style retirement plan. At the time of the legacy funds closure, it was well-funded, but the state wanted to move the majority of the liability to public employees. The new hybrid plan also increased the retirement age, increased employee contributions, reduced the benefit multiplier, and started a defined contribution plan for newly hired public employees. Here is how employee and employee cost break down (source: treasury.tn.gov).

Tennessee’s hybrid plan is set up to give the fund manager the ability to take drastic steps in case of a market downturn or poor fiscal-year performance. According to the Tennessee Treasurer’s Office, if the employer contribution increases above four percent, due to poor performance, the fund manager has the ability to freeze plan benefits, increase employee contributions by one percent, and freeze COLAs. These types of controls are not in the best interest of public employees, who contribute their own money each and every paycheck into their retirement. This Tennessee-style reform of cost-sharing puts a tremendous burden on employees and will cost the state more in the long-term.

Pension plans continue to be the best retirement option for public employees and for lawmakers looking to save money. According to a study by the National Institute on Retirement Security (NIRS) entitled, Still a Better Bang for the Buck, pension plans “deliver the same retirement income at a 48 percent lower cost than 401(k)-type defined contribution accounts.” In the long term, pension funds are less expensive than any other retirement account provided to public employees, even Tennessee’s hybrid account. NIRS cites three reasons why this is a fact: “Pensions only have to save for the average life expectancy of a group of individuals, they are ‘ageless’ and therefore can perpetually maintain an optimally balanced investment portfolio, and they achieve higher investment returns as compared to individual investors because they have lower fees and are managed by investment professionals.”

It is important for lawmakers to use caution when exploring cost-sharing models. Well-funded systems, such as Tennessee’s, are not an appropriate application for all pension plans. Most importantly, lawmakers need to do the one thing most states neglected for years: pay your actuarial required contributions every year, just like public employees pay into their plans each and every year. If Tennessee had decided to stick with their pension plan for public employees, keeping contribution rates into the fund the same, they would have maintained their funding while providing a more secure benefit for their public employees.

{kind=link}